April 10, 2026

by David Maddux, CEO | CIO

We mailed the following note to clients on January 26th.

Three Year Rally Continues to Broaden Across Risk Assets – Have Investors Grown Too Complacent?

Last year at this time I made the case that a 4%+ bond yield was a great rate to lock in, which is now looking pretty attractive as the Fed continued to cut. I also made a fresh case that large US stocks were on the over-valued side. After a slide into the tariff announcements in April, most every sub-group of the US stock market ended the year favorably. International did even better. Although large US stocks are up in price, they are actually no more over-valued than they were as earnings of the companies grew more than I expected.

I would like to cover the following in this letter:

- Four Pillars of Investing

- Markets

- Brightwater Core Model Portfolio – valuations and posture

- New Client Portal (we upgraded our internal “stack” the last two years)

- Followup on my community nudging

Four Pillars of Investing

I have read two books recently and really enjoyed the latest edition of William Bernstein’s Four Pillars of Investing, which he updated after 20 years. Bernstein was a practicing neurosurgeon whose second act is an investment advisor and author. He is committed to rigorous research and also writing in English for regular, interested investors.

The four pillars are 1) Investment Theory, 2) Investment History, 3) Investment Psychology and 4) Business or Vehicles of Investing. His key insights are valuable and I included a short excerpt at the end^, but what has my attention is #3 – Investment Psychology or knowing thyself.

Ideally, we would know ourselves before embarking on investing, but similarly to life overall, we may need to experience investing to really know ourselves in that space. The inspiration here is really wanting to help make sure clients / investors make it through an elongated valley in the stock market and other risky and thus volatile assets, whenever that time comes around.

Stock markets decline at least 10% about once per year on average, but drop more than 20% only about once every four years on average (Ned Davis Research). These normal setbacks are not frequent, but they can test portfolios and emotions. Three recent examples of deeper declines:

- 2022–2023 was a jolt for many as it was 24 months before a new high price in the stock market with a 27% drawdown in the first 9 months.

- 2020 was a dramatic recovery within 7 months following the decline of 35% in the initial COVID panic.

- 2008 was an engulfing experience that dragged down most risky assets and it took stocks 56 months to recover the old high price after a 58% decline.

I do not have a view that we are in for any specific downside scenario, but do think it is important to use all time highs in the stock market (near or at all time high valuations based on many different valuation methodologies) to affirm how much of the stock market I or any client needs to own.

My own crucible was in 2001—before 9/11—in electric utility stocks of all things (utility stocks are classically stodgy and I thought of them as “safe”). Like many things in life, we are not always sure what we learn from our successes, but our failures are obvious challenges to re-evaluate and apply for the better going forward. I am glad to share the play by play, but in short, even though I was young and had time at my side, I invested more than I should have and did so into a sleepy corner of the stock market that got caught up in some unique industry challenges in the middle of a three year decline in the broad stock indices.

Although I thought I knew it all at 26, I clearly still had a lot to learn about myself and the stock market, which is an expensive place to get that education. Three lessons were —

- Allow for a margin for error (in an investment and in a portfolio);

- The magic of compounding is truly magical, but takes time and de facto patience;

- “Everyone gets what they want out of the market.” – Ed Seykota. In other words, we bring our desires, fears and any baggage around money beliefs to our investing.

Markets – So What Now?

My take on the current environment is that valuations still remain exceptionally high, risk levels are high or underpriced and the economy is mixed (unemployment rising and Fed cutting rates), but “okay” per Atlanta Fed’s GDPNow estimate of 5.0% annualized growth for the 4th quarter and the political news is all over the place.

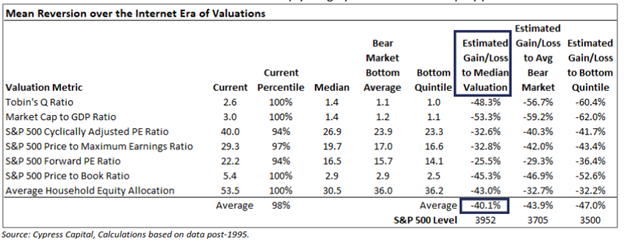

One of the counter arguments to my historical overvaluation case is that the US has entered a new era of exceptionalism since the 1990’s and that the valuations prior to that time period are not relevant to today.

The following table from Cypress Capital research is only measuring data since 1995 and reflects seven different metrics around US stock valuations. Even with this tightened window, a move from the 98th percentile of valuation back to the 50th percentile or “median valuation” would require a roughly 40% decline in stock prices, all else being equal (for example if earnings did not grow further).

A label for this state of being could be called “exuberance.” Maybe this state has been rational vs. irrational as cash yielded 0% for years on end, but my take continues to be that a 4% cash world that swiftly entered the scene in 2022 has not been fully digested.

The other book I read, 1929: Inside the Greatest Crash in Wall Street History—and How it Shattered a Nation by Andrew Ross Sorkin, was recommended by a newer client and I could not put it down (one learning was about Herbert Hoover – I had not appreciated how skilled he was on several fronts and how successful he had been in business). Sorkin concludes—

“The antidote to irrational exuberance is not regulation by itself, nor skepticism, but humility—the humility to know that no system is foolproof, no market fully rational, and no generation exempt. The greater the heights of our certainty, the longer and harder we fall.”

I subscribe to a working definition of humility as knowing what my weaknesses or shortcomings are, but also what my strengths are. False self-deprecation is a veil and explicitly not what I am driving toward. Within investing, there are some things that I know and then there are a lot of things I know I do not know and then there is the tension of needing to allow for things that I do not know that I do not know.

Brightwater Core Portfolio – Valuation & Posture

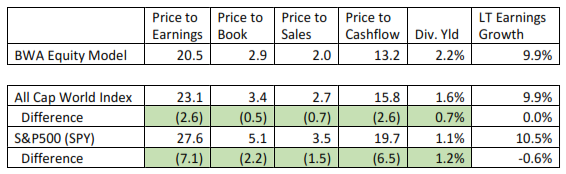

Our Core equity portfolio continues to reflect more favorable valuations compared to the large US proxy of the S&P 500 (38% of the S&P 500’s outcome is from 10 different stocks – four of which are technology and three are communication services—Alphabet Class A, Class C and Meta), as well as the Global All Cap World Index (ACWI), which is made up of about 64% US stocks and 36% International stocks. Its outcome is concentrated in 24% of its largest ten companies. The largest ten stocks underlying the Brightwater portfolio comprise 11% of the mix.

This posture is accomplished by edging slightly away from the largest of the large US companies toward other large US companies showing better values, as well as medium and smaller companies. The Brightwater model is more attractive on each of these traditional valuation metrics and is as follows—

Source: Morningstar Office

Regarding geopolitical considerations like tariffs, politics, oil and war, our approach incorporates their existence and while we care, there is little more to do about it besides visualize “risk” and decide if we can live with it.

We continue to be focused on what we can control, which in this case is implementing a simple, yet robust investment portfolio that barbells risk free interest rates on one end and long-term growth or price appreciation on the other end, rooted in stocks that are fairly priced vs. over-priced.

The next few years could be some kind of muddling through process that is not particularly great, but not particularly bad, of the economy and markets as they navigate whatever cross currents come along. In that kind of environment, fairly priced or attractively priced assets could do just fine over the cycle.

I like this summarization from a recent research piece [emphasis mine]–

“Some of the most successful investors don’t attempt to predict short-term outcomes. They prepare for ranges of outcomes. They build resilient portfolios. They rely on process over prediction. They manage behavior. They stay invested when it feels uncomfortable. They avoid the seduction of perfect foresight.” – Brandon Langley of Blueprint Investment Partners

I regularly review client allocations and also frame them against any investment planning or financial planning we have done, but also know circumstances and biases change and the point is we should be asking the stock allocation question now and not after prices have declined, whenever that will surely occur. Please contact me directly if you want to refresh this look together.

Housekeeping

1099s – I appreciate preparing tax returns early, but also suggest waiting to actually file until early April to avoid the headache of a custodian issuing an Amended 1099. Schwab has shared that they will begin sending theirs out on January 30th, but the last wave will be as late as February 27th.

Client Portal – We have been upgrading and consolidating our technology “stack” the last two years, which has really been useful behind the scenes. A change for clients is a new Client Portal going forward, which we expect to provide better visibility into your assets, better consolidation holistically and better document sharing between us. Sam has done a great job coordinating the two phases to this project and will be sending you an email over the coming days with instructions to activate it.

Community

I shared a motivating piece on the healthy benefits of community in my letter last year and also shared my inspiration to get coffee or lunch with 21 men who live on our street. I was sincerely motivated but on the accountability front I only got together with five of them. I will keep chipping away, but did make more of a point to sit out in front of my house next to the driveway on Saturday mornings – having coffee, reading and emailing. The opportunity has provided more serendipitous conversations with neighbors or others passing by with their dogs or on a walk and has been quite fun. FYI.

In Closing – Grateful

I feel lucky to get to do the work that I do and I know that Misty, Sam, Barry and Katie are all grateful to be able to help make everything happen. I am optimistic about the future, but believe that if we take care of the present, the future will take care of itself.

Taking care of the present involves following a principled investment process. I find deep satisfaction in our focus of helping you tend to your serious money so that you can take care of yourself, which enables you to best take care of your people, whether it be your family, heirs or charities.

I hope 2026 is off to a good start for you and look forward to comparing notes when the opportunity allows.

^I find the following conclusions by Bernstein particularly useful in reminding myself and think they are worth your time–

“Finally, my journey through finance in the two decades since this book’s first edition has taught me more than a few things –

- If you can’t save, it doesn’t matter how well you invest, and an understanding of money’s true utility determines how well you’re able to accumulate it. If you think money’s purpose is to buy stuff, you are doomed to fail, since you’ll quickly find yourself trapped on the ‘hedonic treadmill,’ the insidious evolving hunger for a yet more expensive car, a yet fancier house, or a yet more swish vacation. The best money in the world… is used to buy time and autonomy.

- What one might call the ‘Treasury Bill Theory of Investing Equanimity:’ Your ability to stay the course is directly proportional to the amount of short-term safe assets in your portfolio, denominated in years of living expenses. By far the biggest determinant of your investment success is how well you respond to the worst few percent of times, when the world around you and many of the things you had previously taken for granted melt before your eyes. You will experience such moments at least a few times in your investment career, and nothing will see you through them as well as your T-bills and CDs, no matter how low their yield.

- Volatility, most commonly measured as standard deviation (SD), is a pretty good measure of an asset’s risk, but it lacks a significant dimension: when its losses occur. A classic example is corporate bonds, particularly low-rated, high-yield (“junk”) bonds. A given Treasury security and a given corporate security may have the same SD, but the corporate is a whole lot riskier, since in a financial crisis, you’ll be aching for liquidity to purchase stocks at the fire sale or merely to put food on the table. At such times, corporates will get clobbered, while Treasuries will likely rise in price. [Ed. Note – my initial mentor in this business, my uncle, Frank Cooper, consistently said, “I think you should take your risk in the stock market – not the bond market.” Eg. Buy risk free bonds. My other mentor and business partner, Bob Garey, had long ago embraced this barbell approach of embracing volatility on one side of the portfolio and stability on the other with zero gray space in between. He also showed me the way.]

- The essence of investing is not maximizing returns, but rather maximizing the odds of success, defined as funding retirement, educational expenses, a house down payment, or endowing charities and heirs. Maximizing returns and maximizing the odds of success are two entirely different animals [Ed. Note – Emphasis mine].”

This letter is tonal in nature. We use model portfolios and apply consistent thinking, but each client has a separate account and there are many reasons for exceptions, like tax basis, heirloom holdings, preferences, size of the account, etc. Data source for stock market proxies and representative portfolios: Morningstar Office.

Brightwater Advisory, LLC is an SEC registered investment adviser with its principal place of business in Tampa, Florida. This letter contains general information pertaining to our advisory services. The information is not suitable for everyone and should not be construed as personalized investment advice. This letter contains certain forward-looking statements which indicate future possibilities. Due to known and unknown risks, other uncertainties and factors, actual results may differ materially from the expectations portrayed in such forward-looking statements. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing involves risk, including risk of loss, which an investor must be prepared to bear. We manage investments based upon factors which may include, but are not limited to, a client’s investment time horizon, income, net worth, attitude toward risk and investment knowledge. Therefore, it is important for clients to inform us promptly if there is a substantive change to his or her risk capacity, including financial situation. In addition, if goals and objectives have changed, please let us know immediately. Indices are unmanaged. Any reference to a market index is included for illustrative purposes only as it is not possible to directly invest in an index. For additional information about us, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure web site.

Past performance is no guarantee of future results.

*Registration as an investment adviser does not imply any level of skill or training.

")

")